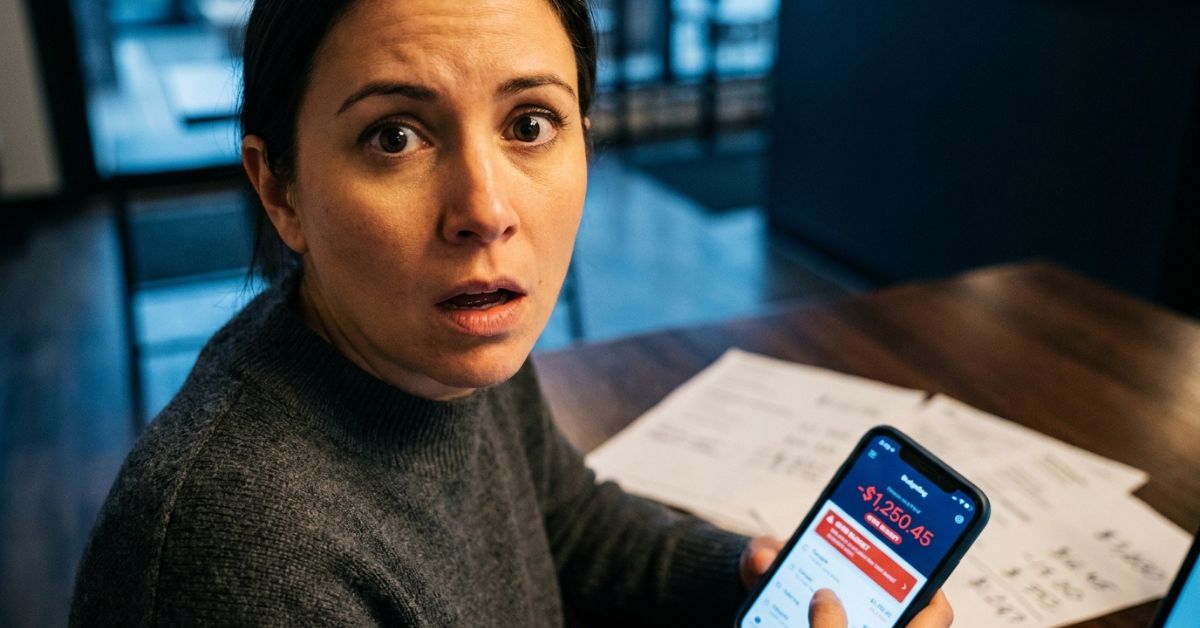

I sat across from a woman who made $85,000 a year and couldn’t explain where $1,200 disappeared every month.

She had a budget. A detailed one, actually. Color-coded spreadsheet, expense categories, the works. She checked it religiously every Sunday morning with her coffee.

And she was still broke.

“I don’t understand,” she said, her voice cracking slightly. “I write everything down. I track everything. But every month, I’m scrambling. Every month, I’m pulling from savings or hitting the credit card.”

I’ve been a financial planner for over a decade, and I’ve seen this exact scenario play out hundreds of times. Smart people. Organized people. People who genuinely want to succeed with money.

All making the same invisible mistake.

Here’s what I’m going to show you: Your budget isn’t broken. You are. But not in the way you think.

The Day I Realized Everyone’s Been Doing Budgets Wrong

Let me take you back to 2019.

I thought I had my financial life together. I’m a financial planner, for crying out loud. I teach this stuff. I had my budget perfectly mapped out, every dollar accounted for.

Then our emergency fund evaporated in six weeks.

Car repair: $1,400. Unexpected dental work: $890. A family obligation that required last-minute flights: $1,200.

None of these were surprises. Not really. Cars break down. Teeth need work. Life happens.

But they weren’t in my budget.

I had done what almost everyone does. I budgeted for the regular stuff—rent, groceries, utilities, Netflix. The things that show up like clockwork.

I completely ignored the irregular expenses that show up just as reliably, just less predictably.

And that realization changed everything about how I teach budgeting.

Your Budget Is a Map. But You’re Driving Without an Engine.

Here’s the thing nobody tells you about budgets.

Having a budget is like having a map to a destination. You know where you are. You know where you want to go. You’ve even highlighted the route.

But you’re standing there holding the map with no car.

The budget shows you the what. What you earn, what you spend, what you want to save.

But it doesn’t give you the how. How money actually moves through your life. How you prevent overspending without thinking about it. How you stop making the same financial mistakes on repeat.

That’s where the cash flow system comes in.

Think of it as the engine. The budget is your map, but the cash flow system is the finely-tuned machine that actually gets you from point A to point B.

Most people spend years perfecting their map while driving a broken-down engine.

The Three Innocent Mistakes That Are Draining Your Bank Account

Mistake #1: The Invisible Expense Blindspot

Pull out your calendar right now. Look at the next twelve months.

How many birthdays are coming up? Anniversaries? Holidays you celebrate?

When’s your car registration due? When was your last dental checkup? (And when do you actually need to schedule the next one?)

I had a client who budgeted $2,800 monthly. Perfect on paper.

Then March hit: her wedding anniversary, her daughter’s birthday, Easter, and her car registration.

One month. Four “irregular” expenses. $1,600 she hadn’t planned for.

“These aren’t irregular,” I told her. “They happen every single year. They’re as regular as your mortgage. You’re just pretending they’re not.”

Our brains love comfort. They love predictability. So we conveniently forget about the expenses that don’t fit our neat monthly pattern.

We budget for groceries and rent. We ignore Valentine’s Day and brake pads and that concert we know we’ll want tickets to.

Mistake #2: The Optimistic Spending Fantasy

Here’s an uncomfortable truth: You spend more than you think you do.

I know you do because I do. Because everyone does.

We tell ourselves we spend $400 a month on food. Then we check our transactions and it’s actually $680.

We say we barely spend anything on clothes. Then there’s $340 in purchases we justified as “needed.”

I had someone insist they spent “maybe $50 a month” on coffee and eating out.

Their transactions? $280.

This isn’t about judgment. This is about honesty.

You cannot fix what you refuse to see.

Pull your last three months of bank statements. Actually look at the numbers. Every purchase. Every transaction.

What you think you spend and what you actually spend are two different budgets.

And you can only make one of them work.

Mistake #3: Ignoring Your Financial Regrets

This one’s uncomfortable, but it’s the most powerful.

What financial mistakes have you made in the last two years?

Not to shame you. Not to make you feel bad.

To learn from them.

I have a client—successful lawyer, brilliant woman—who would go on shopping sprees when she felt stressed. Not wild, reckless spending. Just… more than intended.

She’d feel guilty for weeks afterward.

“Why do you think you do it?” I asked her.

Long pause.

“I think… I feel like I deserve something nice. Like I work so hard, and a new outfit or a nice dinner is my reward.”

“Okay. So let’s budget for that.”

Her face changed. “Wait, what?”

“You’re going to feel stressed. It’s going to happen. Let’s create a category in your budget called ‘Stress Relief Fund.’ Put $200 a month in it. When you feel that urge, you have permission to spend it. Guilt-free.”

She started crying.

Because for the first time, someone told her she wasn’t broken for wanting nice things. She just needed a system that accounted for her actual human behavior.

The Five-Account System That Makes Budgeting Automatic

Here’s where everything changes.

Stop trying to track every dollar in your head. Stop relying on willpower.

You need a system that does the heavy lifting for you.

Account #1: Your Everyday Account

This is where your paycheck lands. This is where your regular expenses come out.

Rent. Groceries. Gas. Subscriptions. Phone bill.

The daily, weekly, fortnightly, monthly stuff.

Most of your money lives here. It comes in, it goes out, repeat.

Simple.

Account #2: Your Financial Float (The Game-Changer)

This is the account that changes everything.

Every time you get paid, you move a small amount into this account.

This is where you stockpile cash for those “irregular” expenses that demolish your budget.

Car registration. Quarterly energy bills. Annual insurance. That dental checkup you’ve been avoiding.

Instead of being blindsided when they arrive, you’ve been preparing for months.

You’re building up a buffer. A cushion. A shield against the expenses that always feel like surprises but never actually are.

Start with whatever you can. $50 a paycheck. $100. Whatever doesn’t break your everyday account.

The goal? Get $3,000 to $10,000 sitting in this account, depending on your life situation.

Sounds like a lot? It’s not when you realize it’s protecting you from debt, from panic, from raiding your savings every time life happens.

Account #3: Your Emergency Fund

Once your everyday account is stable and your float is building, you add this.

This isn’t for car registrations or birthday gifts.

This is for true emergencies. Job loss. Medical emergency. Major home repair.

The stuff you can’t predict and can’t plan for.

Most experts say 3-6 months of expenses. I say start with $1,000 and build from there.

Pro tip: If you have a mortgage, use an offset account or redraw facility. Your emergency money saves you interest while sitting there waiting for the emergency that hopefully never comes.

Account #4: Your Lifestyle Fund (The Joy Account)

This is the account that makes the whole system sustainable.

You can’t just survive. You have to live.

This is for the holiday you’re dreaming about. The concert tickets. The weekend away.

Not essentials. Not emergencies.

Pure. Joy.

Every paycheck, a small amount goes here. You watch it grow. You feel excited instead of deprived.

When you hit your goal, you spend it guilt-free.

Because you planned for it. You earned it. You deserve it.

Account #5: Your Financial Goals Account

This is the empowerment account.

Maybe you’re not sure what you want yet. That’s fine.

Put money here anyway.

Learning about investing? Money’s ready when you’re ready to start.

Considering a side business? Seed capital is waiting.

Want to buy your first property? Down payment is growing.

This account proves to you, every single month, that you’re not just surviving.

You’re building something.

Why This System Works When Willpower Fails

Here’s the beautiful part.

Once this system is running, you stop thinking about budgeting.

You’re not white-knuckling your way through the month, trying to remember what you can and can’t spend.

The system decides for you.

Money comes in. It automatically splits into the right accounts.

Your bills come out of your everyday account.

Your car registration pulls from your float.

Your holiday withdraws from your lifestyle fund.

You’re not resisting temptation. You’re following a system that already accounted for your humanity.

It’s like switching from a manual transmission to automatic.

Same destination. Way less exhausting.

The Woman Who Finally Stopped Hemorrhaging Money

Remember the woman from the beginning? The one losing $1,200 every month?

We spent an hour going through her calendar. Every birthday, every celebration, every predictable “irregular” expense for the next twelve months.

We totaled it up: $8,400 in expenses she had been treating as surprises.

Then we divided by twelve: $700 per month.

“So every month,” I told her, “you need to put $700 into your float account. Not spend it. Just move it there.”

She looked deflated. “But I barely have enough for my regular expenses now.”

“No,” I said gently. “You think you barely have enough. But the reality is you’ve been spending that $700 anyway. You’ve just been scrambling and stressing and using credit cards to cover it.”

“We’re not adding an expense. We’re making an invisible expense visible. And giving you a system to handle it without panic.”

Three months later, she texted me.

Her car needed new tires. $640.

Old her would’ve spiraled. Would’ve put it on a credit card. Would’ve felt like a failure.

New her? Checked her float account. Transferred the money. Paid cash.

“I can’t believe I’m saying this,” her text read, “but I wasn’t even stressed. The money was just… there.”

What Happens When You Finally Get This Right

Once your system is running, something shifts.

You stop living month-to-month.

You stop feeling guilty about spending.

You stop being terrified of checking your bank balance.

Instead, you start seeing opportunities.

“Oh, I’m spending $180 a month on subscriptions I don’t use. That could go to my investment account.”

“I got a $3,000 bonus. My system’s already running smoothly, so this goes straight to my house deposit fund.”

“We want to take a family trip next summer. Let’s start putting $150 a month in the lifestyle account now.”

You’re not scrambling. You’re strategizing.

You’re not surviving. You’re building.

And when life throws you a curveball—because it will—you don’t crumble.

You check which account covers it and move on.

The Part No One Talks About

Here’s what surprised me most about teaching this system.

It’s not just about money.

It’s about self-trust.

Every time you stick to your system, you prove to yourself that you’re capable.

Every time your float account covers an irregular expense, you prove you can plan ahead.

Every time your lifestyle fund lets you take that trip without guilt, you prove you deserve good things.

You’re not just building wealth.

You’re building evidence that you can trust yourself with money.

And that changes everything.

Your Move

You have two choices.

Keep doing what you’re doing. Keep budgeting the way everyone budgets. Keep getting surprised by the same expenses. Keep feeling like you’re failing at something everyone else seems to have figured out.

Or try something different.

Grab your calendar. List every expense coming in the next twelve months.

Pull your bank statements. Face the real numbers.

Write down your financial regrets. Learn from them instead of repeating them.

Then set up your accounts. Start with just two: everyday and float.

Put whatever you can into that float. Even $30 a paycheck.

Watch it grow.

Watch your stress shrink.

Watch yourself transform from someone who’s “bad with money” to someone who has a system that works.

You don’t need to be smarter. You don’t need to earn more.

You just need to stop driving without an engine.

The map’s been there all along.

It’s time to build the machine that actually gets you where you want to go.